While it is easy to get carried away in a day to day gyrations of the stock markets, it is always wise to not miss the forest for the trees. Macro and valuations are as important as the charts and price patterns that guide us on a day to day basis.

Today we will take a look at the various valuation parameters of the major indexes and the some key stocks in the index and some growth names that are market favorites. I won’t be detailing all the key indexes here. Details would be of S&P 500 while other indexes would be explained by way of a simple chart.

S&P 500: One key matrix and highly overlooked during times like these, especially the euphoric times of 2020-21 is the PE ratio, or Price to Earnings ratio. The reason, this very basic, simple, yet important valuation gets missed out is the way people want to chase the price in a euphoria and not to get too concerned when such ratios give us warning signs. Since most of my readers are retail traders, I would be explaining some of these terminologies in a very simple language so that its easier on such readers.

PE – Price to Earnings ratio means at what price a particular stock or index trading at relative to its earnings. There are two ways to look at a PE ratio, one is based on past earnings (many a times called as TTM or Trailing Twelve Months) and another is based on Forward or future earnings. For the simplicity of our analysis, I would be looking at the TTM earnings here and not the future or forward earnings because I consider the future to be uncertain, especially so in given times of high inflation, supply chain constrained macro scenario.

For those who want to look at detailed explanation of how to calculate PE, can refer to investopedia’s website for detailed understanding.

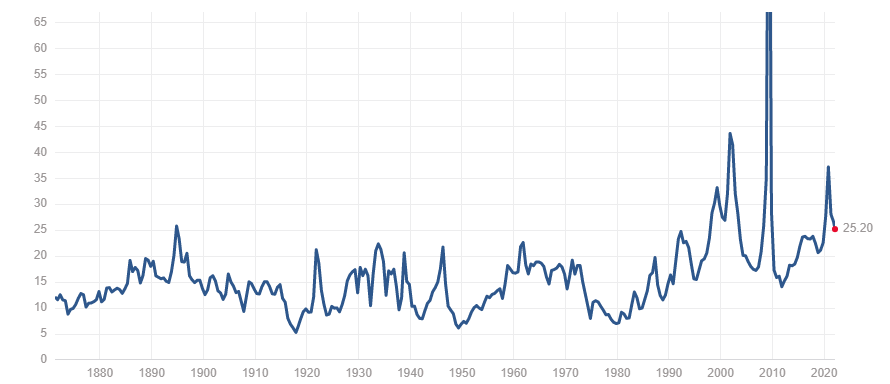

Lets look at the PE valuation of S&P 500 in the following chart:

Currenytly, S&P 500 is trading at 25.2 times its TTM earnings. Is that cheap, expensive or fair? Last 40 years’ analysis based on this chart suggests, its definitely not cheap. We will have to exclude the PE of Jan 2009, when the valuation seemed way too expensive based on the 2008 (Great Financial Crisis) earnings, because the year 2008 was when the earnings were depressed due to the crisis. After excluding that, the valuation, in no ways is cheaper. Rather it is far more expensive and deserves to be sold into.

Fair valuation, from my experience, would be 15-16 times TTM earnings. Which means the valuation itself needs to correct about 50% from here. That can happen, by either price correcting or earnings improving or both. One can only expect and hope for the earnings to improve by such a huge margin in current economic scenario. I would expect earnings to improve by 15% and prices to do the rest.

One important thing worth noting here, though, when markets tend to correct the abnormalities or excesses, it does so beyond the fair value. Hence, I wouldn’t be surprised to see valuation taking deeper than 15X dive to give us a good buying opportunity. You can view the detailed table here

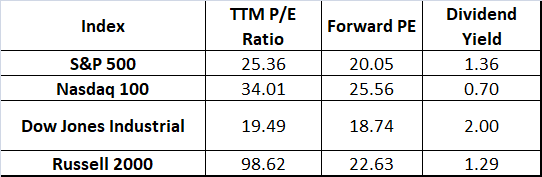

All the major indexes and their key valuation metrics:

Conclusion: In the next 12-18 months, expect S&P 500 to fall anywhere between 30-50% while earnings do the catch up and valuations become worth buying into.

Some key stocks: While valuation does matter for major indexes, it is important to noted that indexes comprise of stocks and their valuation parameters can not be ignored if we are taking a call on the indexes at large.

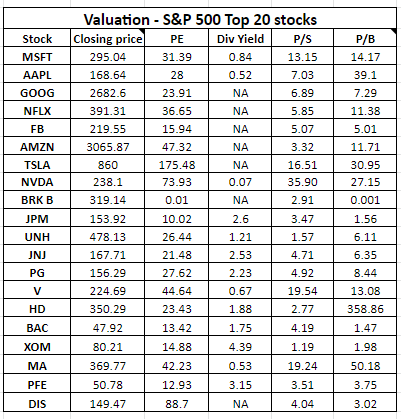

Here’s a table that shows some key valuation matrix of top 20 stocks in S&P500:

No matter what the technical day to day price action might suggest, a close look at some of the valuation matrix of key S&P 500 stocks does not reveal any pretty picture. Although some stocks like NFLX, FB have corrected a lot based on their recent quarterly earnings (and still not very cheap), there are many others such as MSFT, TSLA and AMZN which are highly expensive even after the recent correction no matter which valuation parameter you look at. Having said that, there are other stocks too such as PFE and XOM , that look appealing and need to be grabbed.

I plan to prepare a list of stocks which are worth grabbing at current valuations in the next article, along with technical price action that suggests at what price the risk ratio would be worth entering into. Till then, beware of the richly priced stocks out there.

Leave a comment