Over the past 2 years and more so since 2021 and the after effects of pandemic driven supply crunch, a lot has changed on the global macro economic front. While the global economy did shrink and bounce back, thanks mainly to the central banks driven monetary stimulus, the excesses created by them are hauntig us in many different ways.

- Skilled labour shortage

- Supply crunch of the key resources

- Too much money following too little goods and services

- Housing boom.

- Very low interest rates.

While, many of those issues are not new and have been ongoing ever since the Great Financial Crisis of 2008-09, yet it got only excerbated due to the pandemic induced excesses. Since a lot has been written already on all those topics, I won’t be taking much of my time in talking about those and would rather go directly to the crux of the subject: In economic parlance, where do we go from here?

The journey till now has been easy, despite the fact that the Fed was way behind the curve early on. Pandemic driven supply crunches and the low base driven inflation shocks have taken us so far that the inflationary components have turned out to be sticky. Common man is reeling under the high gas, rent and grocey prices even as the Fed is raising rates to ensure the flow of money is curtailed to buy already expensive goods and services.

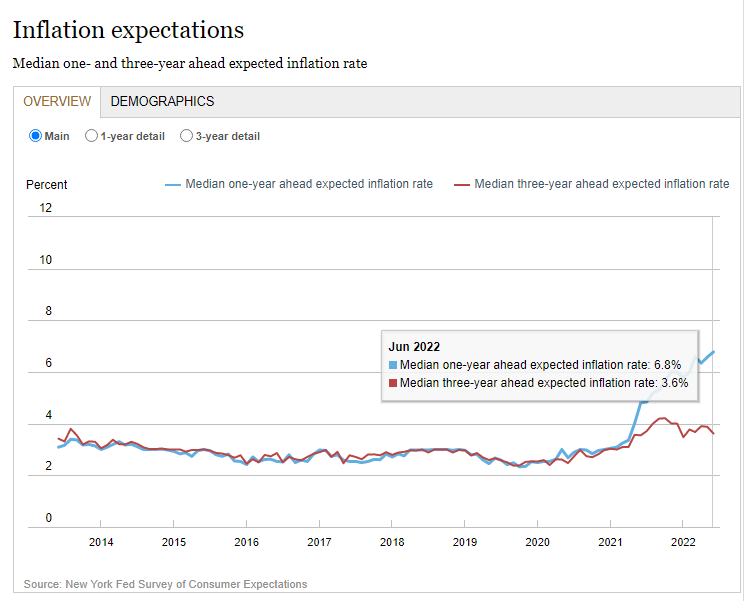

In other words, common man is stuck between a rock and a wall wherein he’s being crushed on both the sides – lack of money sypply and higher prices at the store. Latest NY Federal Reserve survey for the consumer inflation expectations released in July (for the month of June) shows the true picture of what consumers expect:

The median one-year-ahead inflation expectation increased to 6.8 percent in June, up from 6.6 percent in May, a new series high. Inflation expectations at the medium and longer term posted a decline. The median expected one-year-ahead change in home prices dropped sharply to 4.4 percent, from 5.8 percent in May. Median year-ahead household spending growth expectations retreated from a series high in May, declining 0.6 percentage point to 8.4 percent but remaining well above its 2021 average of 5.0 percent. Households’ assessments of their current financial situation deteriorated in June as more respondents reported being financially worse off than they were a year ago.

source: Federal Reserve Bank of New York.

Given this backdrop, it makes me wonder if markets’ expectations of interest rates peaking sometime end of 2022 or start of 2023. Yes, inflation and inflationary expectations are dynamic in nature and given recent drop in commodity prices, chances are even these expectatoins of 6.8% would need to be corrected in the coming months. But expecting these numbers to fall sharply within Fed’s target of 2% would be foolhardy.

Fed is expected to raise rates all the way upto 3-3.5% by the end of this year and if we have to include July 27th rate hike, we are already at 2.5% Fed Funds rate, which means Fed would be raising rates by a maximum 50-100 bps, as per markets’ expectations – which seems quite low, in my opinion.

For the Fed to be able to kill inflatoin expectations (and inflatoin too), it would have to raise rates to a minimum of 150-200bps more. Simply because the interest rates of 3.5% is already in the price and mindsets of the general consumer even as they fret these skyrocketing prices. The mindset behind higher inflationary expectation which is at a four-decade high, would need actions which are beyond normal. Fed rates of 3-4% would not curtail the behaviour of the consumer who is used to excessive spending due to highly available money supply over the past 15 years and more so, since the pandemic.

The Fed can not make a mistake of breathing a sigh of relief just because commodity prices have cooled off recently. The policy mistakes of considering inflation as transitory and allowing it to run hot without taking any actions are still costing markets and economy very dearly. Because if commodity prices surge again and so does inflationary expectations, it would lead to economic growth to come crashing down along with continued higher inflation – a so called stagflationary situation. At the same time, if the Fed indeed continues to raise interest rates while maintaining hawkish stance, it would lead to deflationary situation in the long run – something that has its own dire consequences.

Chances are that the Fed is already on course to make another policy mistake – assuming that the economy is not in a recession and the one can be avoided. Here’s why: The yield curve, which is usually seen as a sign of looming recession has already been sending warnig signs for weeks and months now (for the starters – a yield curve is formed by the difference in yields between various tenures of the bonds. You can read more about the yield curve on this webpage of investopedia). Here’s a Reuters article that explains the whats and wheres of the yield curve: Analysis: U.S. yield curve flashing more warning signs of recession risks ahead.

Considering that the Fed is on another misstep already, there is every likelihood of the Fed making a mistake of slowing down the pace of rate hikes (as noted today in the press conference already). If so, the Fed risks sending the economy into the dangers of stagflation as the inflation would turn its face higher along with sending economic growth into the tailspin slowdown.

Although, I am not an economist and I don’t claim to be expert of macro economics either, but given the scenarios we are in, I’m really not sure if the Fed is equipped enough (mentally) to ride us through the rough rides of higher inflationary scenarios along with lower economic growth. The monetary tools of the past (such as QE and the Operation Twist) won’t do any favour in such an economic backdrop and the only thing that would work is being aggressively hawkish to curb inflation and inflationary expectations. The comments the Fed made today on recession and the strength of the economy seems to be just about right retroactively, not proactively.

We need proactive Fed that drives the market and not driven by the market. The Fed that sees what is lying ahead and not to what has already happened. When the Fed said today that they would react to the incoming data and act accordingly, it signalled us that it is handicapped and does not want to be proactive to perceive oncoming macro-economic dangers and would rather be happy in claiming victory after the event as against guarding us from the very event of stagflation.

Leave a comment