Over the last 2 years we have seen inflation surging up all the way to 40-year highs of more than 8 percent to back around 5 percent. Much has been talked about the supply chain dynamics of the inflation, which seemed to have abated and about employment side of the debate – sticky employment, sticky growth (so far, barring the recent GDP numbers). But there hasn’t been much talk or debate about the productivity side of the goods and services being produced.

Today, we try and nibble into the productivity side of the inflation dynamics and see if there is anything that’s worth looking at and has not been talked about?

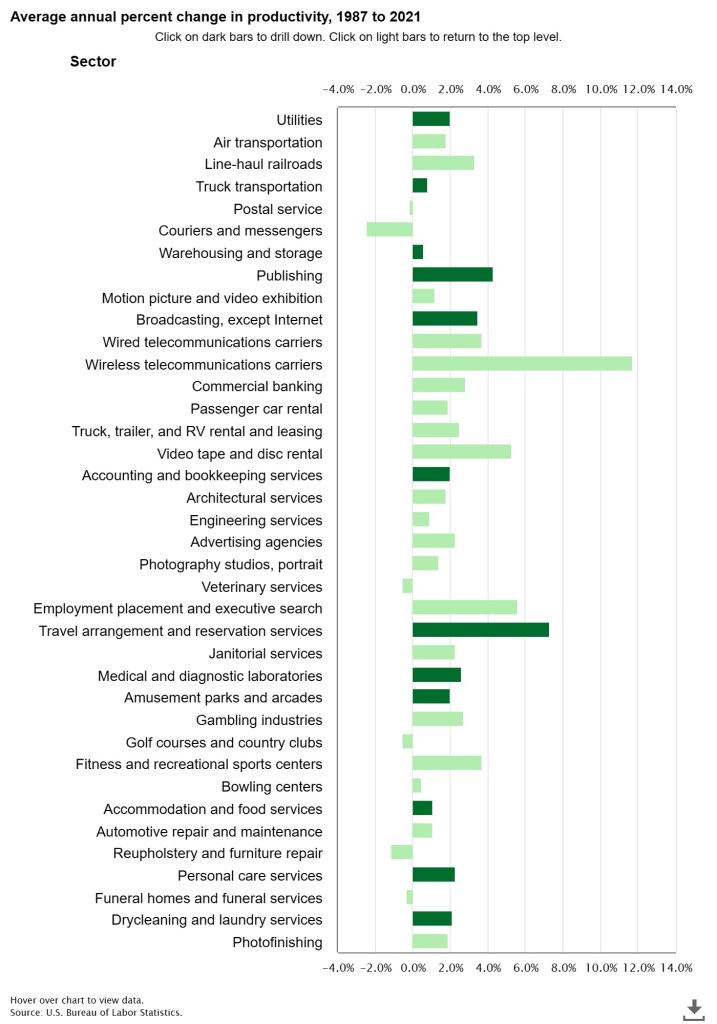

Embedded below are a few charts that portray how has productivity been in various industries. What is interesting is while, employment numbers have been robust in the last couple of years, productivity as a whole for the past few decades, hasn’t seen much of a rise in some key industries.

Truck transportation, postal services, couriers and messengers, warehousing and storage, automotive maintenance and repair are some key sectors that have seen either negative growth or very sluggish growth in productivity.

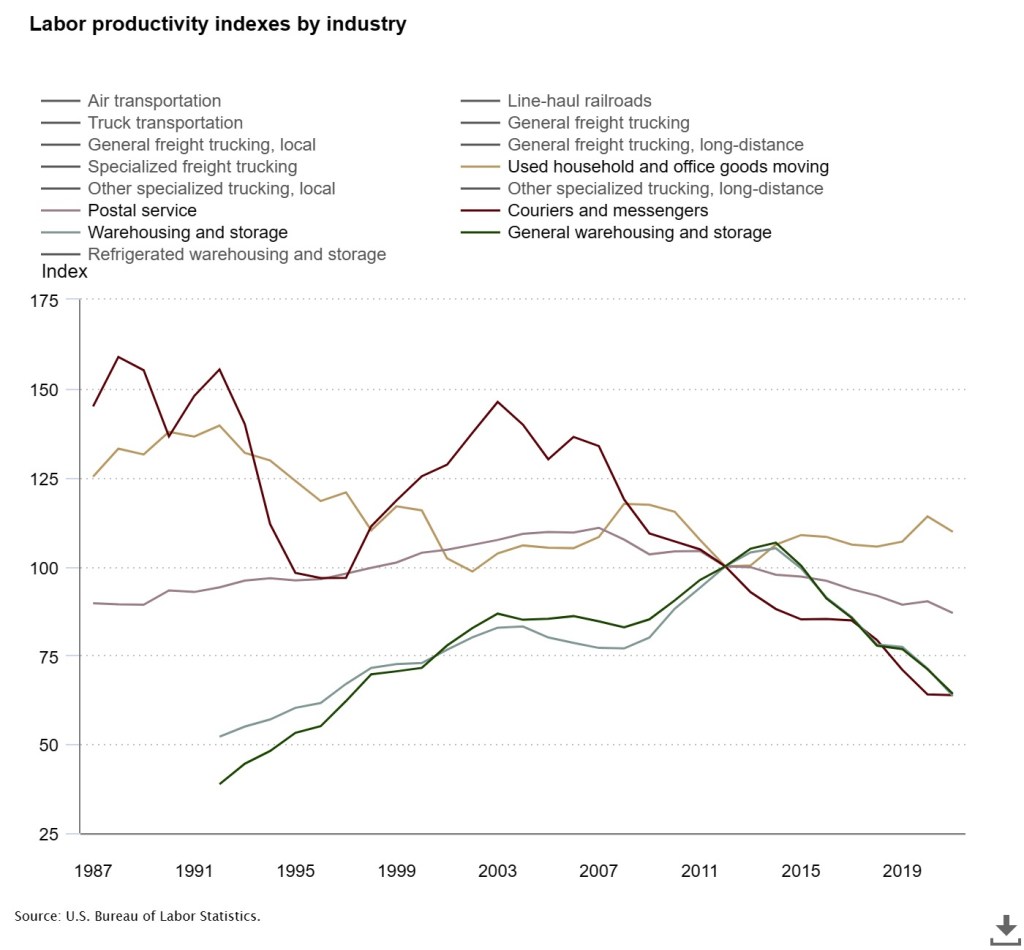

Even when we look at labor productivity of those industries in particular, we notice why it has been so. Labor productivity itself is the cause of concern for these sectors that has led to negative growth of productivity.

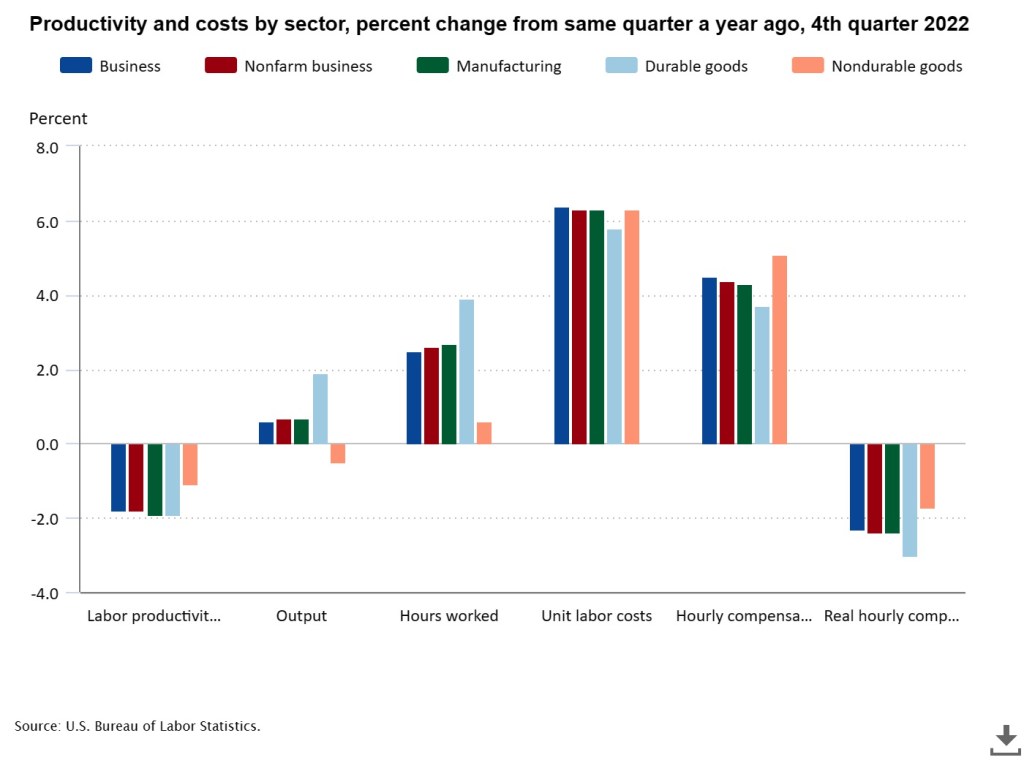

From the latest data point perspective, for the fourth quarter of 2022, labor productivity has seen negative growth while unit labor costs have seen more than 6 percent growth p.a. in almost all the sectors, exacerbating the inflation issue, while hourly compensation has seen around 4 percent growth p.a.

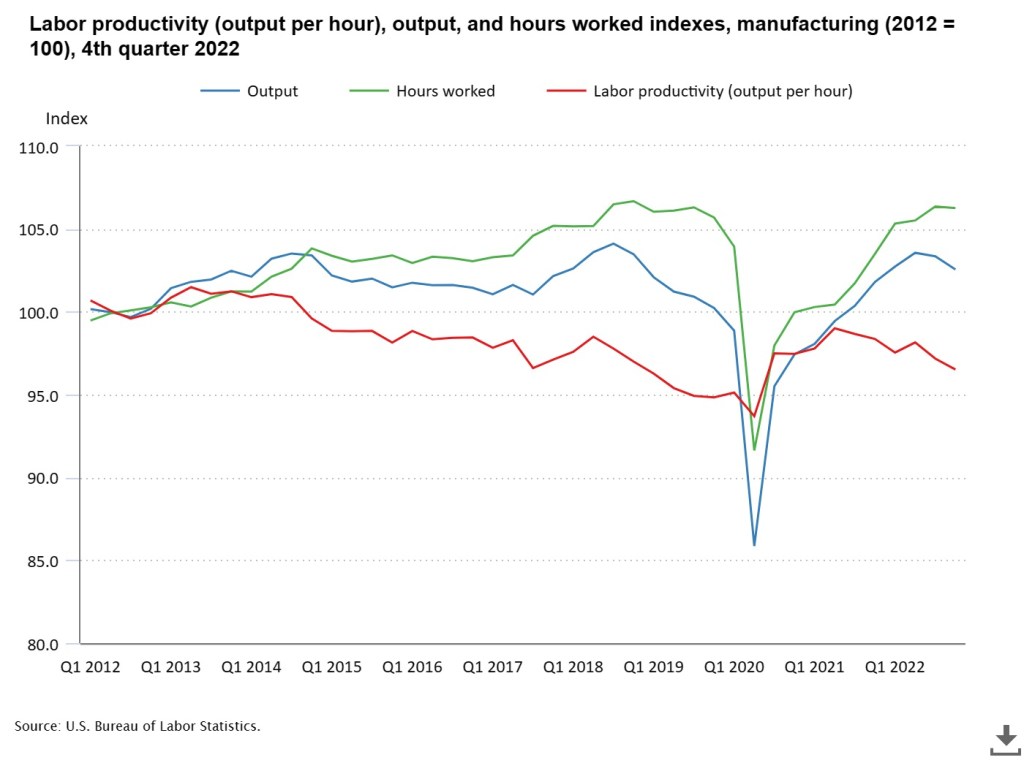

In the last 10-years, labor productivity per hour has seen negative growth even as hours worked have grown up.

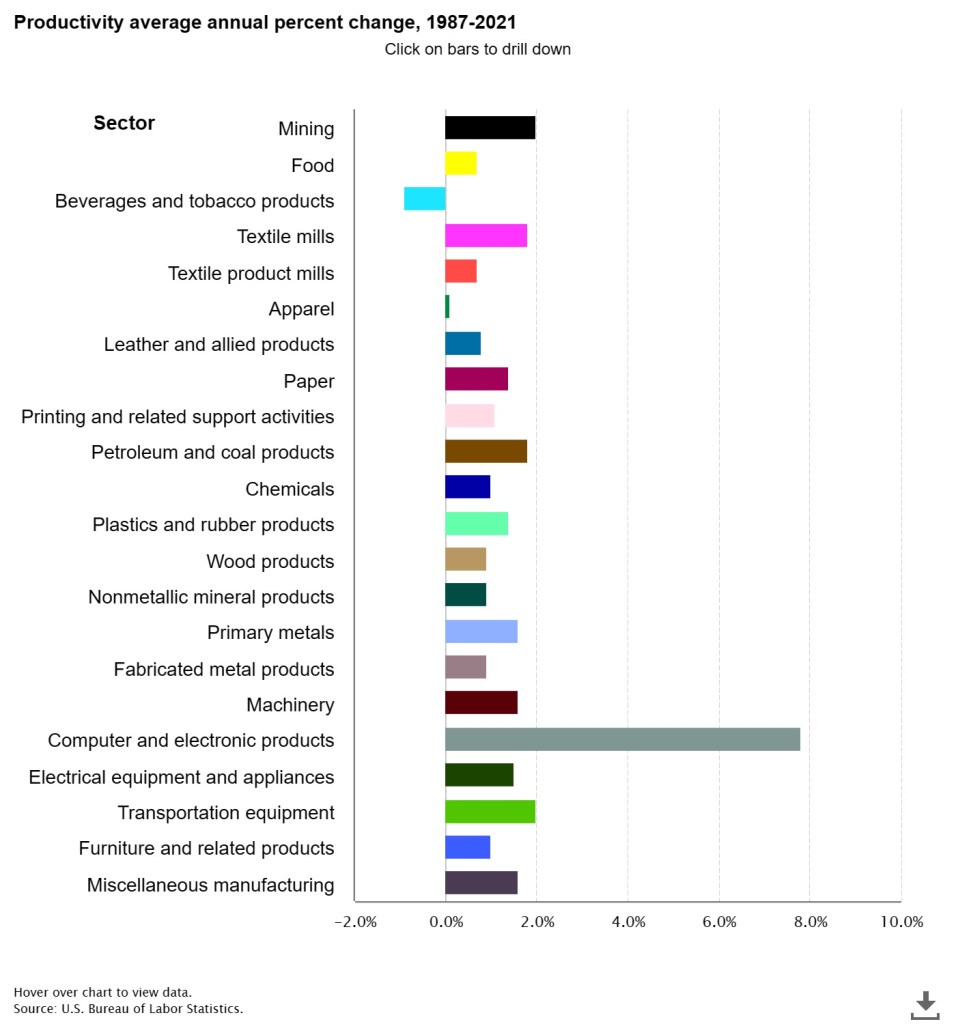

Here’s another graph that portrays which industries have seen productivity rising and which haven’t. Clearly Technology has been a bystander – Seeing annual average growth of nearly 8 percent since 1987, beating all the other sectors.

Inflation is not just about the demand of the goods and services being produced, but is also about the supply of those goods and services. Supply, while it is about how many of those actual products are being produced, that quantity depends on the productivity of the labor and the processes involved. While there are many sectors and industries that have seen productivity rising, there still are some key sectors such as warehousing, which have not been able to maintain higher productivity rise in their processes and services.

While, Fed has been trying hard to cater to the demand side of the problem by making supply of money expensive affair, it has not been able to curtain the employment numbers, which the Fed has been desperately trying to. Why? Because companies are struggling to maintain productivity from the very labor, the Fed doesn’t want to have employed. End result – More demand for labor to produce the same amount of goods and services. Making the job even harder for the Fed to contain inflation.

Irrespective of what the Fed has done and will continue to do, the inflation story is NOT about the demand of the goods, it is and will continue to be the supply side of the story.

Leave a comment